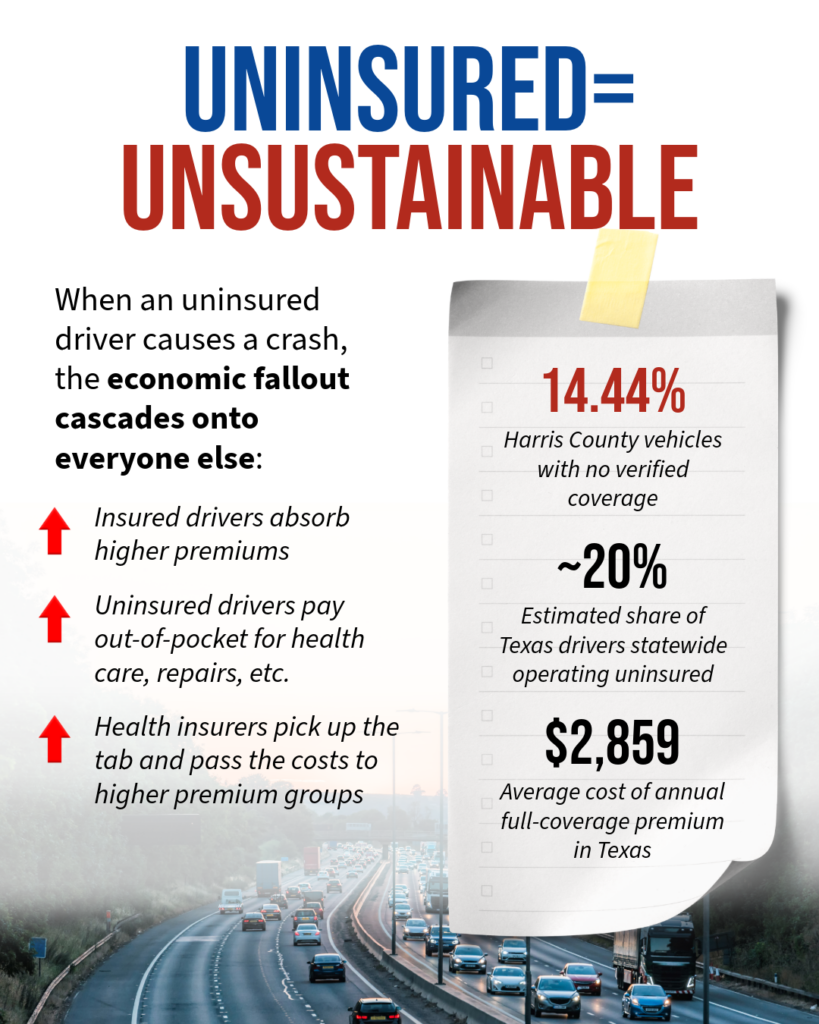

A recent study found that 14.44% of Harris County vehicles lack verified insurance coverage due to rising costs, with average annual premiums at roughly $2,856 per vehicle. Statewide, researchers estimate approximately 20% of Texas drivers are uninsured. Rising costs are part of the problem; going without is likely to make insurance less affordable for everyone else.

Auto insurance prices rose 23.8% in 2022, and 25.5% in 2023, and Texas drivers now pay an average of $2,859 per year for full coverage. When forced to choose between premiums and rent, many families simply drop auto insurance coverage, creating serious public safety risks and shifting costs onto every insured driver in the state.

What is driving premiums to these levels? Legitimate cost pressures (inflation, repair costs, severe weather) account for some of it. But the Texas Legislature must reckon with a harder truth: the state’s litigation environment is a significant and addressable contributor.

Between 2009 and 2023, Texas led the nation with 207 verdicts exceeding $10 million, totaling more than $45 billion in damages. In 2024 alone, Texas recorded 23 nuclear verdicts — more than any other state — generating $3 billion in awards. Auto accident cases account for roughly 23% of all nuclear verdicts nationally. These outsized awards feed directly into higher premiums for every Texas driver.

Compounding the problem is Third-Party Litigation Funding (TPLF), which allows outside investors, including some backed by foreign governments, to bankroll lawsuits in exchange for a share of the payout. U.S. The TPLF industry reached $16 billion in 2024. TPLF delays settlements, inflates verdicts, and operates with zero transparency in Texas, where there are currently no disclosure requirements. Other stats, and even the federal government, have proposed taxing the TPLF industry or, at least, requiring transparency when TPLF is involved in a case.

The Texas Legislature has the authority to change that. Last session, Texans for Lawsuit Reform championed a bill directly targeted at inflated medical damage claims and sought to restore fairness to the civil justice system. Back in 2023, Florida’s new tort reform law dropped that state from the second-highest nuclear verdict jurisdiction in the country to tenth. New companies entered the market, boosting competition. Carriers cut premiums by 7-20% and returned $1 billion back to drivers and homeowners — all proof that legislative action works.

The Texas Legislature must prioritize lawsuit reform, TPLF disclosure, and standardized medical damage calculations as core public policy goals. Affordability and accountability are two sides of the same coin. Until lawmakers in Austin act, the uninsured driver crisis will only deepen as the affordability gap gets wider.